The Power of Loan Insurance: In today’s fast-paced financial landscape, securing a loan can be a pivotal step toward achieving personal or professional goals, whether it’s buying a home, starting a business, or funding education. However, life is unpredictable, and unforeseen events like job loss, illness, or economic downturns can jeopardize your ability to repay a loan.

This is where loan insurance steps in as a critical tool for safeguarding your financial future. In this comprehensive guide, we’ll explore the role of loan insurance, its benefits, types, costs, and how it can provide peace of mind for borrowers. By the end, you’ll understand why loan insurance is an essential component of responsible financial planning.

What is Loan Insurance?

Loan insurance, also known as credit insurance or loan protection insurance, is a type of insurance designed to cover loan repayments in the event that a borrower is unable to make payments due to specific circumstances. These circumstances often include job loss, disability, critical illness, or even death. By mitigating the financial risks associated with borrowing, loan insurance ensures that your loan obligations are met, protecting both you and your lender from default.

Loan insurance can be applied to various types of loans, including personal loans, mortgages, auto loans, and business loans. It acts as a safety net, ensuring that your financial commitments are honored even during challenging times, thereby preventing damage to your credit score or the loss of valuable assets like your home or car.

Why Loan Insurance Matters

Borrowing money comes with inherent risks. Economic instability, health issues, or unexpected life events can disrupt your ability to make timely loan payments. Without a backup plan, missed payments can lead to penalties, a damaged credit score, or even foreclosure or repossession. Loan insurance mitigates these risks by covering your payments under specific conditions, offering the following key benefits:

- Financial Security: Loan insurance provides a buffer against financial hardship, ensuring that your loan repayments are covered during periods of unemployment, illness, or other qualifying events.

- Credit Score Protection: By preventing missed payments, loan insurance helps maintain your credit score, which is crucial for future borrowing and financial opportunities.

- Peace of Mind: Knowing that your loan obligations will be met, even in tough times, reduces stress and allows you to focus on recovery or rebuilding.

- Asset Protection: For secured loans like mortgages or auto loans, loan insurance can prevent the loss of your home or vehicle due to default.

- Support for Loved Ones: In the event of a borrower’s death, some loan insurance policies cover the outstanding loan balance, relieving family members of financial burdens.

Types of Loan Insurance

Loan insurance comes in several forms, each designed to address specific risks associated with borrowing. Understanding the different types can help you choose the policy that best suits your needs. Here are the most common types of loan insurance:

1. Credit Life Insurance

Credit life insurance is designed to pay off the remaining balance of a loan if the borrower passes away. This type of insurance ensures that your loved ones are not left with the burden of repaying your loan, protecting them from financial strain. It’s commonly offered for mortgages, auto loans, and other large loans.

2. Credit Disability Insurance

Credit disability insurance covers loan payments if the borrower becomes disabled and is unable to work. This type of insurance typically kicks in after a waiting period and provides coverage for a specified duration, helping you stay current on your loan while you recover.

3. Credit Unemployment Insurance

Credit unemployment insurance covers loan payments if the borrower loses their job involuntarily. This is particularly valuable during economic downturns when job security may be uncertain. Coverage is usually limited to a certain number of payments or a specific time frame.

4. Credit Property Insurance

For secured loans like auto or home loans, credit property insurance protects the collateral (e.g., your car or house) against damage or loss. This ensures that the lender’s investment is secure, even if the underlying asset is compromised.

5. Mortgage Payment Protection Insurance (MPPI)

Specifically designed for homeowners, MPPI covers mortgage payments in the event of job loss, illness, or disability. This type of insurance is critical for preventing foreclosure and maintaining homeownership during financial hardship.

How Does Loan Insurance Work?

Loan insurance policies vary depending on the provider and the type of loan, but the general process is straightforward:

- Purchase the Policy: Loan insurance is often offered by lenders at the time of borrowing, though you can also purchase it from third-party insurers. Be sure to compare policies to find the best coverage and rates.

- Pay Premiums: Premiums can be paid as a lump sum upfront or as part of your monthly loan payments. The cost depends on factors like the loan amount, term, and your risk profile.

- File a Claim: If an event covered by the policy occurs (e.g., job loss or disability), you file a claim with the insurer. You’ll need to provide documentation, such as medical records or proof of unemployment.

- Receive Benefits: Once approved, the insurer will either make loan payments directly to the lender or pay off the remaining loan balance, depending on the policy.

Factors to Consider When Choosing Loan Insurance

Before purchasing loan insurance, it’s important to evaluate your needs and the policy’s terms. Here are some key factors to consider:

- Coverage Scope: Ensure the policy covers the specific risks you’re concerned about, such as job loss, disability, or death.

- Cost vs. Benefit: Compare the cost of premiums to the potential financial protection offered. In some cases, building an emergency fund may be a more cost-effective alternative.

- Exclusions and Limitations: Read the fine print to understand what’s not covered, such as pre-existing medical conditions or voluntary unemployment.

- Loan Type: Some policies are tailored to specific loans, like mortgages or auto loans, so choose one that aligns with your borrowing needs.

- Lender Requirements: Some lenders may require loan insurance for high-risk borrowers or large loans, so check if it’s mandatory.

The Cost of Loan Insurance

The cost of loan insurance varies based on several factors, including:

- Loan Amount: Larger loans typically have higher premiums because the insurer’s potential payout is greater.

- Loan Term: Longer loan terms may result in higher premiums due to the extended risk period.

- Borrower’s Risk Profile: Factors like age, health, and employment stability can influence premium costs.

- Type of Coverage: Comprehensive policies that cover multiple risks (e.g., death, disability, and unemployment) tend to be more expensive.

On average, loan insurance premiums range from 1% to 5% of the loan amount, though this can vary. For example, for a $10,000 loan, you might pay $100 to $500 in premiums over the loan term. To keep costs manageable, shop around for quotes from multiple insurers and consider whether you need all the coverage options offered.

Is Loan Insurance Worth It?

The value of loan insurance depends on your financial situation and risk tolerance. Here are some scenarios where loan insurance may be particularly beneficial:

- High Debt-to-Income Ratio: If a large portion of your income goes toward loan payments, insurance can provide a safety net during financial disruptions.

- Unstable Employment: If you work in a volatile industry or have concerns about job security, unemployment insurance can protect you.

- Limited Savings: If you don’t have an emergency fund to cover loan payments during tough times, loan insurance can prevent default.

- Dependents: If you have a family that relies on your income, credit life or disability insurance can protect them from inheriting your debt.

However, loan insurance may not be necessary for everyone. If you have substantial savings, a stable income, or other forms of insurance (like life or disability insurance), you may not need additional loan protection. Carefully weigh the costs and benefits to make an informed decision.

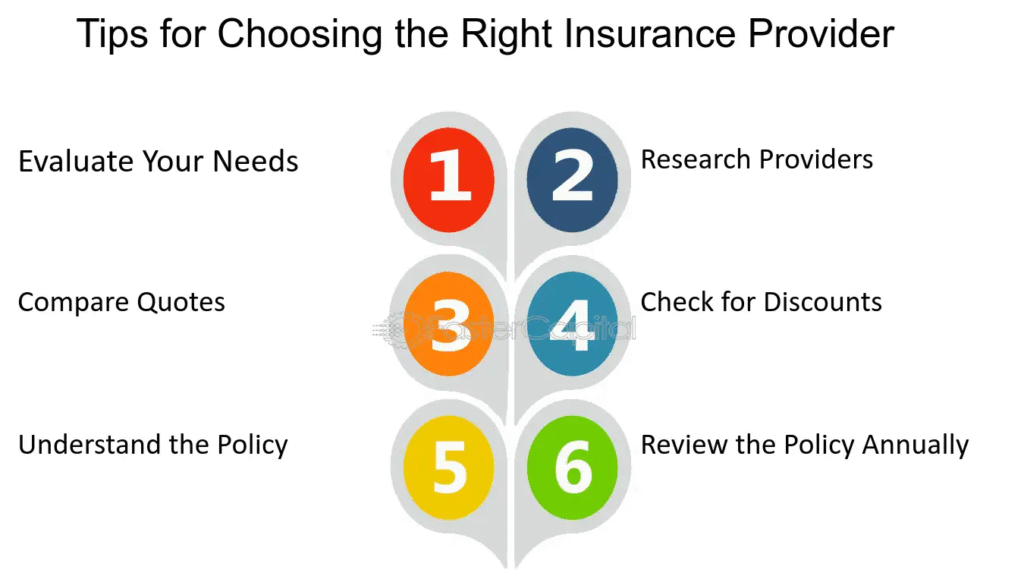

How to Choose the Right Loan Insurance Policy

To select the best loan insurance policy, follow these steps:

- Assess Your Needs: Identify the risks you’re most concerned about, such as job loss or health issues.

- Compare Providers: Research insurers and compare coverage options, premiums, and customer reviews.

- Read the Policy Terms: Understand what’s covered, what’s excluded, and any waiting periods or limitations.

- Consult a Financial Advisor: If you’re unsure, a financial advisor can help you evaluate whether loan insurance fits into your overall financial plan.

- Check for Alternatives: Consider whether other insurance policies or an emergency fund could provide similar protection at a lower cost.

Common Misconceptions About Loan Insurance

Despite its benefits, loan insurance is often misunderstood. Here are some common myths debunked:

- Myth 1: Loan Insurance is Mandatory: While some lenders require it, loan insurance is often optional. Always check with your lender.

- Myth 2: It Covers All Loans: Not all policies cover every type of loan. Ensure the policy matches your loan type and needs.

- Myth 3: It’s Always Expensive: Premiums can be affordable, especially if you shop around or opt for limited coverage.

- Myth 4: It’s Redundant if You Have Other Insurance: While life or disability insurance may offer similar benefits, loan insurance is specifically tailored to cover loan payments.

Conclusion

Loan insurance is a powerful tool for protecting your financial future, offering peace of mind and security in an unpredictable world. By covering loan payments or paying off balances during challenging times, it helps you avoid default, protect your credit score, and secure your assets. However, it’s not a one-size-fits-all solution, so carefully evaluate your needs, compare policies, and consider alternatives before purchasing.

Whether you’re taking out a mortgage, auto loan, or personal loan, loan insurance can be a valuable addition to your financial strategy. By understanding its role and benefits, you can make informed decisions that safeguard your financial stability and ensure a brighter, more secure future.