The Essential Guide to Loan Insurance: In today’s uncertain economic landscape, taking out a loan can be a double-edged sword. While loans provide essential funding for homes, cars, education, or personal needs, they also come with inherent risks. What happens if you lose your job, face a serious illness, or encounter an unexpected financial setback?

These scenarios can lead to missed payments, damaged credit scores, and even asset repossession. This is where loan insurance steps in as a critical tool for mitigating loan risks. Also known as credit insurance or payment protection insurance, loan insurance acts as a safety net, ensuring your loan obligations are met even during tough times.

This comprehensive guide explores everything you need to know about loan insurance, from its fundamentals to advanced strategies for selection. Whether you’re a first-time borrower or a seasoned financial planner, understanding how loan insurance works can help safeguard your financial future. We’ll cover types, benefits, drawbacks, and tips on choosing the right policy, all while emphasizing its role in risk mitigation.

Understanding Loan Risks: Why Mitigation Matters

Before diving into loan insurance, it’s essential to grasp the risks associated with borrowing. Loans expose borrowers to several potential pitfalls:

- Default Risk: The inability to make payments, leading to penalties, higher interest rates, or legal action.

- Credit Score Damage: Missed payments can lower your credit score, making future borrowing more expensive or impossible.

- Asset Loss: For secured loans like mortgages or auto loans, defaulting could result in foreclosure or repossession.

- Personal Financial Strain: Unexpected events like job loss or medical emergencies can amplify debt burdens, affecting mental health and family stability.

According to financial experts, these risks are amplified in volatile economies, where unemployment rates can spike unexpectedly. Mitigating these through proactive measures, such as insurance, is not just advisable—it’s often crucial for long-term financial security.

Lenders also face risks, including non-payment, which is why they sometimes require or offer insurance options. However, from a borrower’s perspective, mitigating loan risks means protecting your assets and peace of mind. Loan insurance transfers some of this risk to an insurer, providing a buffer against life’s uncertainties.

What is Loan Insurance?

Loan insurance is a specialized policy designed to cover your loan repayments if you can’t make them due to specific covered events. It’s typically offered as an add-on when you take out a loan, but you can also purchase it independently. The insurer pays the lender directly, either covering monthly installments for a set period or paying off the entire loan balance in severe cases.

Unlike general life or health insurance, loan insurance is tied directly to your debt obligation. Premiums are often added to your monthly loan payments, making it convenient but potentially increasing the overall cost. Coverage usually lasts for the loan term or a specified duration, such as 12 to 24 months.

For example, if you’re hospitalized and unable to work, the policy might cover your payments for up to six months, preventing default. This is particularly valuable for high-value loans like mortgages, where the stakes are higher. In essence, it’s a form of risk transfer, shifting the financial burden from you to the insurance provider.

Types of Loan Insurance

Loan insurance isn’t one-size-fits-all; it comes in various forms tailored to different risks and loan types. Understanding these can help you select the most appropriate coverage:

- Credit Life Insurance: This pays off the remaining loan balance if the borrower dies. It’s common for mortgages and personal loans, ensuring your family isn’t burdened with debt. Benefits include peace of mind for heirs, but it only activates upon death.

- Credit Disability Insurance: Also called credit accident and health insurance, this covers loan payments if you’re disabled and unable to work. Payments continue until you recover or the loan is paid off, typically for a limited period like 24 months.

- Involuntary Unemployment Insurance: This protects against job loss, covering payments for a short term (e.g., 3-12 months) while you seek new employment. It’s ideal in unstable job markets but excludes voluntary quits or firings for cause.

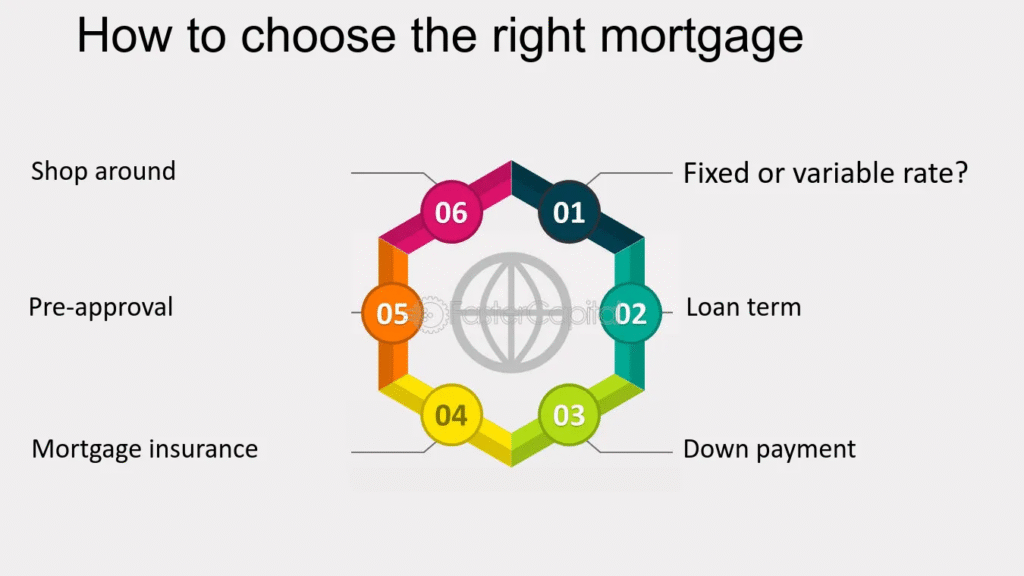

- Private Mortgage Insurance (PMI): Mandatory for conventional mortgages with less than 20% down payment, PMI protects the lender if you default. It’s not for your benefit directly but mitigates your risk by enabling homeownership with a smaller down payment. FHA and USDA loans have similar requirements.

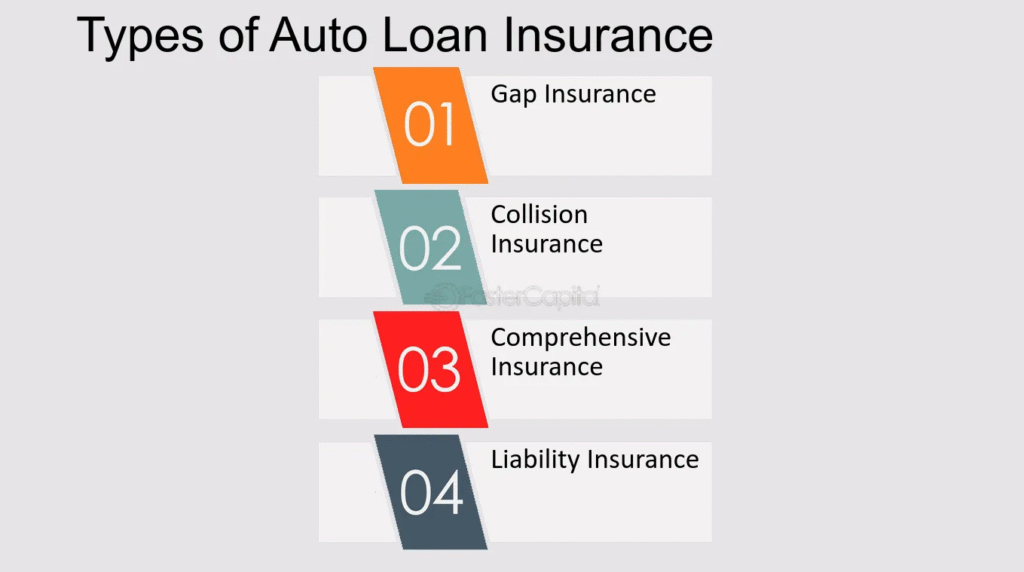

- Property Insurance for Secured Loans: For auto or home loans, this covers damage to the collateral asset. While not “loan insurance” per se, it’s often required to mitigate risks to the lender’s security.

- Gap Insurance: Common for auto loans, this covers the difference between the car’s value and the loan balance if totaled.

Choosing the right type depends on your loan (e.g., personal vs. mortgage) and personal circumstances, like health or job stability.

Benefits of Loan Insurance

Investing in loan insurance offers numerous advantages, making it a key strategy for mitigating loan risks:

- Financial Protection: It ensures payments continue during hardships, preventing default and preserving your credit score.

- Peace of Mind: Knowing your loan is covered reduces stress, especially for sole breadwinners or those with dependents.

- Family Security: In cases of death or disability, it shields loved ones from inheriting debt.

- Easier Loan Approval: Some lenders offer better terms if you opt for insurance, as it lowers their risk.

- Tax Benefits: Certain policies qualify for deductions under tax laws, like Section 80C in some jurisdictions.

- Coverage for Unforeseen Events: From pandemics to economic downturns, it provides a buffer against broad risks.

For instance, during the COVID-19 crisis, many borrowers relied on such insurance to avoid defaults amid widespread job losses.

Potential Drawbacks and Considerations

While beneficial, loan insurance isn’t without downsides:

- Cost: Premiums can add 0.5% to 2% to your loan amount, increasing total repayment. For a $10,000 loan, this could mean hundreds extra.

- Exclusions and Limitations: Policies often exclude pre-existing conditions, voluntary unemployment, or short-term disabilities.

- Not Always Necessary: If you have robust emergency savings, employer benefits, or other insurances (e.g., disability from work), it might be redundant.

- Over-Selling by Lenders: Some providers push expensive policies; shopping independently can save money.

Weigh these against your risk profile. For short-term loans, the cost might outweigh benefits, but for long-term debts like mortgages, it’s often worthwhile.

How to Choose the Right Loan Insurance

Selecting the optimal policy requires careful evaluation:

- Assess Your Needs: Consider loan size, term, and personal risks (e.g., health history, job security).

- Compare Options: Shop from multiple providers, not just your lender. Look at premiums, coverage limits, and claim processes.

- Read the Fine Print: Check exclusions, waiting periods, and payout terms. Ensure it covers key risks like illness or job loss.

- Calculate Costs: Use online calculators to compare total loan costs with and without insurance.

- Seek Independent Advice: Consult financial advisors or use comparison sites for unbiased insights.

- Check for Mandates: For mortgages, verify if PMI is required and when it can be canceled (e.g., at 20% equity).

By following these steps, you can tailor insurance to effectively mitigate your specific loan risks.

Alternatives to Loan Insurance

If loan insurance doesn’t fit, consider these risk mitigation strategies:

- Build an Emergency Fund: Aim for 3-6 months of expenses to cover payments during setbacks.

- Diversify Income Sources: Side gigs or investments can provide backup.

- Employer Benefits: Many jobs offer disability or unemployment coverage.

- Refinancing or Consolidation: Lower payments through better terms.

- General Insurance Policies: Life, health, or income protection plans often overlap with loan-specific coverage.

These alternatives can be more cost-effective, especially if combined.

Conclusion: Secure Your Financial Future with Smart Risk Mitigation

Mitigating loan risks through insurance is a proactive step toward financial stability. By understanding types like credit life and disability insurance, weighing benefits against costs, and choosing wisely, you can protect yourself from the unforeseen. Remember, the goal is not just to borrow but to borrow smartly—ensuring loans enhance your life without becoming a burden.

In an era of economic unpredictability, loan insurance offers invaluable protection. Consult professionals, compare options, and integrate it into your broader financial plan. With the right approach, you can navigate loans confidently, knowing your risks are mitigated.